You might be using an unsupported or outdated browser. To get the best possible experience please use the latest version of Chrome, Firefox, Safari, or Microsoft Edge to view this website.

We independently select all products and services. If you click through links we provide, we may earn a commission.

Learn More.

Colin Beresford is a writer and editor experienced in helping people make the best decisions with their money, whether it's buying a car or taking on a loan. He has written for Bloomberg, The Associated Press, NerdWallet, Car and Driver magazine, amo...

Colin Beresford is a writer and editor experienced in helping people make the best decisions with their money, whether it's buying a car or taking on a loan. He has written for Bloomberg, The Associated Press, NerdWallet, Car and Driver magazine, amo...

Colin Beresford is a writer and editor experienced in helping people make the best decisions with their money, whether it's buying a car or taking on a loan. He has written for Bloomberg, The Associated Press, NerdWallet, Car and Driver magazine, amo...

Colin Beresford is a writer and editor experienced in helping people make the best decisions with their money, whether it's buying a car or taking on a loan. He has written for Bloomberg, The Associated Press, NerdWallet, Car and Driver magazine, amo...

Jordan Tarver has spent seven years covering mortgage, personal loan and business loan content for leading financial publications such as Forbes Advisor. He blends knowledge from his bachelor's degree in business finance, his experience as a top perf...

Jordan Tarver has spent seven years covering mortgage, personal loan and business loan content for leading financial publications such as Forbes Advisor. He blends knowledge from his bachelor's degree in business finance, his experience as a top perf...

Jordan Tarver has spent seven years covering mortgage, personal loan and business loan content for leading financial publications such as Forbes Advisor. He blends knowledge from his bachelor's degree in business finance, his experience as a top perf...

Jordan Tarver has spent seven years covering mortgage, personal loan and business loan content for leading financial publications such as Forbes Advisor. He blends knowledge from his bachelor's degree in business finance, his experience as a top perf...

Financial and loans expert Joel Larsgaard loves nerding out on the topic of personal finance with the mission of helping others improve their financial standing.

He has been in the money media space for almost 20 years. He produced "...

Financial and loans expert Joel Larsgaard loves nerding out on the topic of personal finance with the mission of helping others improve their financial standing.

He has been in the money media space for almost 20 years. He produced "...

Financial and loans expert Joel Larsgaard loves nerding out on the topic of personal finance with the mission of helping others improve their financial standing.

He has been in the money media space for almost 20 years. He produced "...

Financial and loans expert Joel Larsgaard loves nerding out on the topic of personal finance with the mission of helping others improve their financial standing.

He has been in the money media space for almost 20 years. He produced "...

Editorial Note: We earn a commission from partner links on Forbes Advisor. Commissions do not affect our editors' opinions or evaluations.

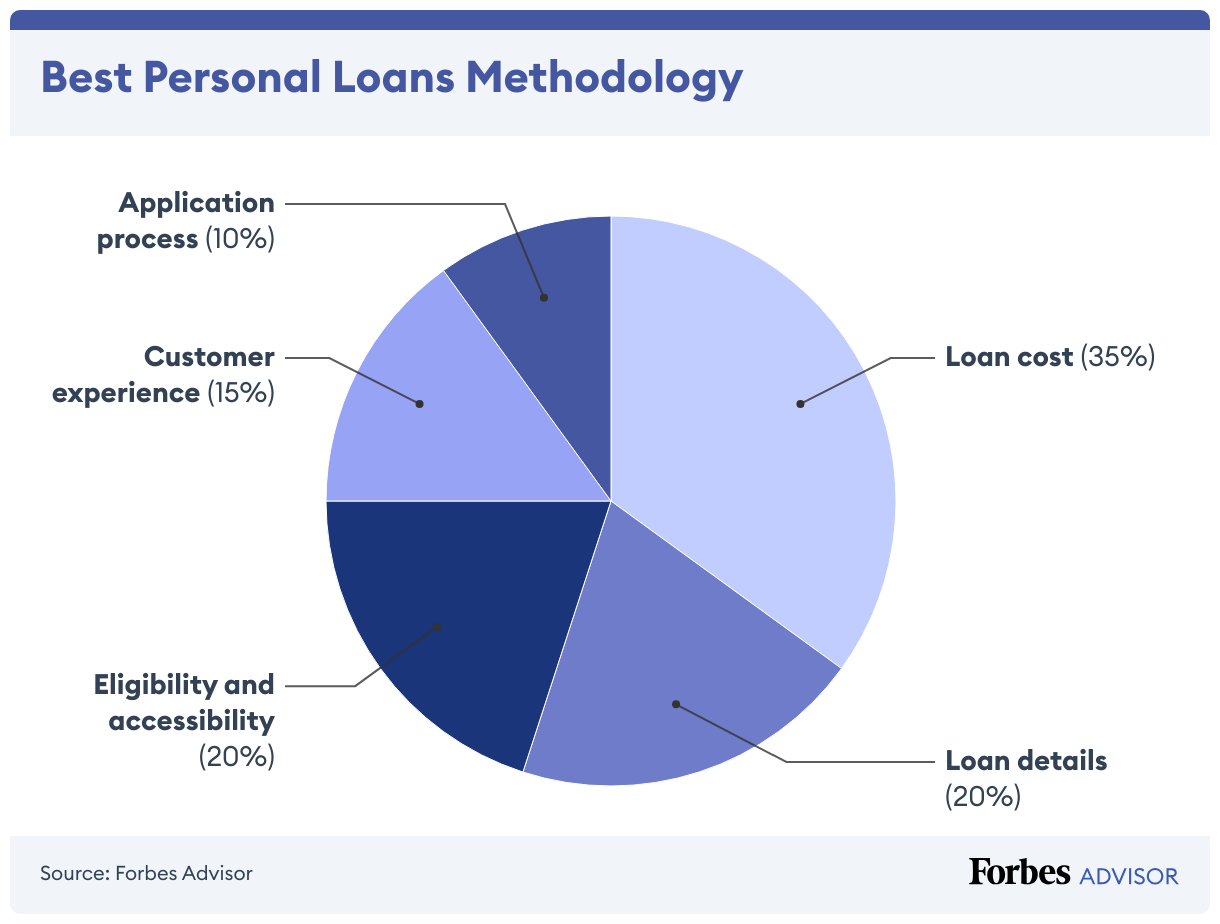

When searching for a personal loan, we understand you need sufficient financing at an affordable price. To find the best personal loan options for you, we compared 29 national lenders and researched 16 data points in five different categories.

Loan cost was the largest determining factor since this impacts every borrower, but we also considered other loan features when ranking lenders.

Our editors are committed to bringing you unbiased ratings and information. Advertisers do not and cannot influence our ratings. We use data-driven methodologies to evaluate financial products and companies, so all are measured equally. You can read more about our editorial guidelines and the personal loans methodology for the ratings below.

29 nationwide lenders researched

16 data points evaluated and scored

Unbiased editorial team

No AI writing

Best Personal Loans of 2025

Best for Good to Excellent Credit

SoFi®

5.0

Our ratings take into account loan cost, loan details, eligibility and accessibility, customer experience and application process. All ratings are determined solely by our editorial team.

SoFi is an online lender that offers a range of products, including large personal loans that you can use for various purposes.

Why We Like It

SoFi’s personal loans come with higher maximum amounts and longer terms than loans from other lenders.

What We Don’t Like

SoFi requires a minimum credit score of Does not disclose and an annual income of at least $45,000, making it out of reach for some borrowers.

Who It’s Best For

If you need a large loan amount and a long loan term, a SoFi personal loan is a great option if you can meet the borrower requirements.

Consumer Sentiment Index

4.2

4.2/10

Consumer Score

The Consumer Sentiment Index from Forbes Advisor uses a proprietary weighting system designed by our subject matter experts. It evaluates thousands of consumer insights and reviews from leading online forums to determine customer satisfaction at scale.

Consumer Sentiment Index

3,184

How do we calculate

We gather and analyze consumer sentiment from a range of sources to create the Consumer Sentiment Index to determine customer satisfaction levels for each feature outlined below. This data is designed to give you an idea of real consumer experience of the services and product we review. This data is currently separate from our overall rating out of 5

Insights Analyzed

#

Interest Rates and Fees

ForInterest Rates and Fees

57% of people had positive sentiments

14% of people had neutral sentiments

29% of people had negative sentiments

57%

14%

29%

ForInterest Rates and Fees

57% of people had positive sentiments

14% of people had neutral sentiments

29% of people had negative sentiments

#

Customer Service

For Customer Service

26% of people had positive sentiments

11% of people had neutral sentiments

63% of people had negative sentiments

26%

11%

63%

For Customer Service

26% of people had positive sentiments

11% of people had neutral sentiments

63% of people had negative sentiments

#

Loan Terms and Flexibility

For Loan Terms and Flexibility

56% of people had positive sentiments

23% of people had neutral sentiments

21% of people had negative sentiments

56%

23%

21%

For Loan Terms and Flexibility

56% of people had positive sentiments

23% of people had neutral sentiments

21% of people had negative sentiments

#

Ease of Approval and Process

For Ease of Approval and Process

64% of people had positive sentiments

10% of people had neutral sentiments

26% of people had negative sentiments

64%

10%

26%

For Ease of Approval and Process

64% of people had positive sentiments

10% of people had neutral sentiments

26% of people had negative sentiments

While some borrowers appreciate SoFi’s simple application and disbursement process, others are dissatisfied with communication and customer service. Borrowers are also frustrated with misleading promotional offers and how their loan inquiries were handled.

Pros & Cons

Prequalification without a hard inquiry

Same-day approval possible

Can pay off third-party creditors directly

High credit score requirement

Co-signers not permitted

Details

Eligibility:

Minimum credit score required. Does not disclose

Minimum annual income. $45,000

Co-borrowers. Permitted

Co-signers. Not permitted

Customer service

We evaluated SoFi’s customer service experience by calling its team directly. During our assessment, we found that its wait times were some of the longest—one minute and 41 seconds. Once we connected with customer service, its team was able to answer each of our questions effectively.

They disclosed loan amounts, available interest rates, required documents and loan approval times. They also shared information about prequalification and potential fees.

Best for Bad Credit

Upgrade

4.8

Our ratings take into account loan cost, loan details, eligibility and accessibility, customer experience and application process. All ratings are determined solely by our editorial team.

Minimum Credit Score

600

APR range

Personal loans made through Upgrade feature Annual Percentage Rates (APRs) of 7.99%-35.99%. All personal loans have a 1.85% to 9.99% origination fee, which is deducted from the loan proceeds. Lowest rates require Autopay and paying off a portion of existing debt directly. Loans feature repayment terms of 24 to 84 months. For example, if you receive a $10,000 loan with a 36-month term and a 17.59% APR (which includes a 13.94% yearly interest rate and a 5% one-time origination fee), you would receive $9,500 in your account and would have a required monthly payment of $341.48. Over the life of the loan, your payments would total $12,293.46. The APR on your loan may be higher or lower and your loan offers may not have multiple term lengths available. Actual rate depends on credit score, credit usage history, loan term, and other factors. Late payments or subsequent charges and fees may increase the cost of your fixed rate loan. There is no fee or penalty for repaying a loan early. Personal loans issued by Upgrade’s bank partners. Information on Upgrade’s bank partners can be found at https://www.upgrade.com/bank-partners/.

Personal loans made through Upgrade feature Annual Percentage Rates (APRs) of 7.99%-35.99%. All personal loans have a 1.85% to 9.99% origination fee, which is deducted from the loan proceeds. Lowest rates require Autopay and paying off a portion of existing debt directly. Loans feature repayment terms of 24 to 84 months. For example, if you receive a $10,000 loan with a 36-month term and a 17.59% APR (which includes a 13.94% yearly interest rate and a 5% one-time origination fee), you would receive $9,500 in your account and would have a required monthly payment of $341.48. Over the life of the loan, your payments would total $12,293.46. The APR on your loan may be higher or lower and your loan offers may not have multiple term lengths available. Actual rate depends on credit score, credit usage history, loan term, and other factors. Late payments or subsequent charges and fees may increase the cost of your fixed rate loan. There is no fee or penalty for repaying a loan early. Personal loans issued by Upgrade’s bank partners. Information on Upgrade’s bank partners can be found at https://www.upgrade.com/bank-partners/.

7.99% to 35.99%

$1,000 to $50,000

Editor’s Take

Upgrade is an online lender that offers personal loans along with savings and checking accounts.

Why We Like It

Upgrade offers borrowers small loan amounts with accessible borrower requirements, including a minimum credit score requirement of 600 and no income requirement.

What We Don’t Like

Although Upgrade advertises rates as low as 7.99%, some borrowers could be offered the maximum rate of 35.99%, which is high compared to other lenders.

Who It’s Best For

Upgrade personal loans are best for borrowers with bad credit histories or who may have inconsistent income.

Consumer Sentiment Index

5.4

5.4/10

Consumer Score

The Consumer Sentiment Index from Forbes Advisor uses a proprietary weighting system designed by our subject matter experts. It evaluates thousands of consumer insights and reviews from leading online forums to determine customer satisfaction at scale.

Consumer Sentiment Index

5,884

How do we calculate

We gather and analyze consumer sentiment from a range of sources to create the Consumer Sentiment Index to determine customer satisfaction levels for each feature outlined below. This data is designed to give you an idea of real consumer experience of the services and product we review. This data is currently separate from our overall rating out of 5

Insights Analyzed

#

Interest Rates and Fees

For Interest Rates and Fees

54% of people had positive sentiments

10% of people had neutral sentiments

36% of people had negative sentiments

54%

10%

36%

For Interest Rates and Fees

54% of people had positive sentiments

10% of people had neutral sentiments

36% of people had negative sentiments

#

Customer Service

For Customer Service

67% of people had positive sentiments

3% of people had neutral sentiments

30% of people had negative sentiments

67%

3%

30%

For Customer Service

67% of people had positive sentiments

3% of people had neutral sentiments

30% of people had negative sentiments

#

Loan Terms and Flexibility

For Loan Terms and Flexibility

74% of people had positive sentiments

10% of people had neutral sentiments

16% of people had negative sentiments

74%

10%

16%

For Loan Terms and Flexibility

74% of people had positive sentiments

10% of people had neutral sentiments

16% of people had negative sentiments

#

Ease of Approval and Process

For Ease of Approval and Process

94% of people had positive sentiments

2% of people had neutral sentiments

4% of people had negative sentiments

94%

2%

4%

For Ease of Approval and Process

94% of people had positive sentiments

2% of people had neutral sentiments

4% of people had negative sentiments

Upgrade customers report mixed experiences with its personal loan offerings. Some wins that jump out include the streamlined application process, easy approval and quick funding. But their experiences were not perfect. Some users are dissatisfied with the high APRs and loan fees that make working with Upstart costly.

Pros & Cons

Flexible eligibility requirements

Can pay off creditors directly

High loan amounts available

High APR range

Fees for late payments and insufficient funds

Charges origination fees from 0% and 12%

Details

Eligibility:

Minimum credit score. 600

Minimum income. None

Co-applicants. Permitted

Customer service

We called Upgrade to gauge the responsiveness of its customer service team and found it to be one of the most responsive lenders on our list. While we waited just over one minute for their team to answer our call—which is not the fastest time—they were transparent and knowledgeable about Upgrade’s loans.

We received information on loan amounts, required documentation, interest rate ranges, approval speed, fees and various perks, like hardship programs and autopay discounts. The representative also confirmed that they report payments to credit bureaus.

Disclosure

Personal loans made through Upgrade feature Annual Percentage Rates (APRs) of 7.99%-35.99%. All personal loans have a 1.85% to 9.99% origination fee, which is deducted from the loan proceeds. Lowest rates require Autopay and paying off a portion of existing debt directly. Loans feature repayment terms of 24 to 84 months. For example, if you receive a $10,000 loan with a 36-month term and a 17.59% APR (which includes a 13.94% yearly interest rate and a 5% one-time origination fee), you would receive $9,500 in your account and would have a required monthly payment of $341.48. Over the life of the loan, your payments would total $12,293.46. The APR on your loan may be higher or lower and your loan offers may not have multiple term lengths available. Actual rate depends on credit score, credit usage history, loan term, and other factors. Late payments or subsequent charges and fees may increase the cost of your fixed rate loan. There is no fee or penalty for repaying a loan early. Personal loans issued by Upgrade’s bank partners. Information on Upgrade’s bank partners can be found at https://www.upgrade.com/bank-partners/.

Best for Low Interest Rates

LightStream

4.7

Our ratings take into account loan cost, loan details, eligibility and accessibility, customer experience and application process. All ratings are determined solely by our editorial team.

LightStream is a personal loan lender that offers loans with low interest rates that you can use for a range of purposes.

Why We Like It

LightStream offers loans with interest rates as low as 6.49%, which is one of the lowest minimum interest rates among personal loan lenders. The lender also has a rate-beat program and a 0.50% rate discount for borrowers who enroll in autopay.

What We Don’t Like

Although many personal loan lenders allow borrowers to prequalify with a soft credit inquiry, LightStream doesn’t. To see if you qualify, you’ll need to submit an application and undergo a hard credit check, which temporarily impacts your credit score.

The Consumer Sentiment Index from Forbes Advisor uses a proprietary weighting system designed by our subject matter experts. It evaluates thousands of consumer insights and reviews from leading online forums to determine customer satisfaction at scale.

Consumer Sentiment Index

1,791

How do we calculate

We gather and analyze consumer sentiment from a range of sources to create the Consumer Sentiment Index to determine customer satisfaction levels for each feature outlined below. This data is designed to give you an idea of real consumer experience of the services and product we review. This data is currently separate from our overall rating out of 5

Insights Analyzed

#

Interest Rates and Fees

For Interest Rates and Fees

64% of people had positive sentiments

14% of people had neutral sentiments

22% of people had negative sentiments

64%

14%

22%

For Interest Rates and Fees

64% of people had positive sentiments

14% of people had neutral sentiments

22% of people had negative sentiments

#

Customer Service

For Customer Service

19% of people had positive sentiments

1% of people had neutral sentiments

80% of people had negative sentiments

19%

1%

80%

For Customer Service

19% of people had positive sentiments

1% of people had neutral sentiments

80% of people had negative sentiments

#

Loan Terms and Flexibility

For Loan Terms and Flexibility

71% of people had positive sentiments

18% of people had neutral sentiments

11% of people had negative sentiments

71%

18%

11%

For Loan Terms and Flexibility

71% of people had positive sentiments

18% of people had neutral sentiments

11% of people had negative sentiments

#

Ease of Approval and Process

For Ease of Approval and Process

77% of people had positive sentiments

8% of people had neutral sentiments

15% of people had negative sentiments

77%

8%

15%

For Ease of Approval and Process

77% of people had positive sentiments

8% of people had neutral sentiments

15% of people had negative sentiments

LightStream borrowers appreciate the user-friendly application process, fast funding and competitive interest rates. However, there are a handful of concerns about customer service and discrepancies between advertised and actual rates.

Pros & Cons

Long loan terms available

Low interest rates

Fast approval and funding

No prequalification option

High minimum loan amount

Low average customer rating on Trustpilot

Details

Eligibility:

Minimum credit score. 700

Minimum income. Does not disclose

Co-borrowers. Permitted

Customer service

We tried to call LightStream to test the quality of its customer service, but they don’t provide a customer service number. If you want to reach their customer service team, you must contact them via email. Its email support is available Monday through Friday, 9:30 am to 7 pm and Saturday, 12 to 4 pm ET.

Best for Debt Consolidation

LendingClub

4.1

Our ratings take into account loan cost, loan details, eligibility and accessibility, customer experience and application process. All ratings are determined solely by our editorial team.

LendingClub offers personal loans among other products, including checking and savings accounts and business loans. Its personal loans can be used for various purposes, including consolidating debt.

Why We Like It

LendingClub lets borrowers consolidate from $1,000 to $40,000 in debt and offers direct payoff to creditors. With APRs starting at 7.90% to 35.99%, borrowers consolidating high-interest debt who qualify for the lowest rates can save money on interest payments.

What We Don’t Like

LendingClub charges origination fees of 3% to 8%, which are typically taken out of the total loan amount.

Who It’s Best For

LendingClub’s personal loans are best for borrowers looking to consolidate high-interest debt who want to have creditors paid off directly.

Consumer Sentiment Index

6.0

6/10

Consumer Score

The Consumer Sentiment Index from Forbes Advisor uses a proprietary weighting system designed by our subject matter experts. It evaluates thousands of consumer insights and reviews from leading online forums to determine customer satisfaction at scale.

Consumer Sentiment Index

10,607

How do we calculate

We gather and analyze consumer sentiment from a range of sources to create the Consumer Sentiment Index to determine customer satisfaction levels for each feature outlined below. This data is designed to give you an idea of real consumer experience of the services and product we review. This data is currently separate from our overall rating out of 5

Insights Analyzed

#

Interest Rates and Fees

For Interest Rates and Fees

64% of people had positive sentiments

13% of people had neutral sentiments

23% of people had negative sentiments

64%

13%

23%

For Interest Rates and Fees

64% of people had positive sentiments

13% of people had neutral sentiments

23% of people had negative sentiments

#

Customer Servic

For Customer Service

68% of people had positive sentiments

2% of people had neutral sentiments

30% of people had negative sentiments

68%

2%

30%

For Customer Service

68% of people had positive sentiments

2% of people had neutral sentiments

30% of people had negative sentiments

#

Loan Terms and Flexibility

For Loan Terms and Flexibility

84% of people had positive sentiments

7% of people had neutral sentiments

9% of people had negative sentiments

84%

7%

9%

For Loan Terms and Flexibility

84% of people had positive sentiments

7% of people had neutral sentiments

9% of people had negative sentiments

#

Ease of Approval and Process

For Ease of Approval and Process

95% of people had positive sentiments

2% of people had neutral sentiments

3% of people had negative sentiments

95%

2%

3%

For Ease of Approval and Process

95% of people had positive sentiments

2% of people had neutral sentiments

3% of people had negative sentiments

Borrowers are typically satisfied with LendingClub and value the competitive interest rates and efficient application process. However, some cite concerns about high origination fees and communication issues.

Pros & Cons

Directly pay off creditors with debt consolidation loans

Offers loans as small as $1,000 to $40,000

No minimum credit or income requirements

Charges origination fees

Terms available for two to five years

Details

Eligibility:

Minimum credit score. None

Minimum annual income. None

Co-borrowers. Permitted

Customer service

We tested LendingClub’s customer service to assess how helpful it is for prospective borrowers and found the representative could provide only surface-level answers. For example, after waiting just over one minute to connect with a rep, they confirmed you can set up autopay but did not confirm if any autopay discounts are available. In another case, they mentioned LendingClub charges an origination fee but didn’t disclose anything further like the amount.

However, this does not mean they were not responsive or able to provide helpful information. We connected with a rep in just over one minute. Through our evaluation, we gathered key information, including loan amounts, required documentation such as W-2s and bank statements, loan assistance options and funding turnaround times.

Best for Credit Union Financing

PenFed

4.1

Our ratings take into account loan cost, loan details, eligibility and accessibility, customer experience and application process. All ratings are determined solely by our editorial team.

PenFed is a credit union originally founded for veterans and military members but has since opened its membership to anyone.

Why We Like It

For borrowers looking for a personal loan from a credit union, PenFed stands out for its national presence, low interest rates and flexible membership requirements.

What We Don’t Like

Although PenFed is available in all 50 states, it only operates branches in 14.

Who It’s Best For

PenFed personal loans are best for borrowers who are looking to borrow from a credit union at low interest rates.

Consumer Sentiment Index

3.8

3.8/10

Consumer Score

The Consumer Sentiment Index from Forbes Advisor uses a proprietary weighting system designed by our subject matter experts. It evaluates thousands of consumer insights and reviews from leading online forums to determine customer satisfaction at scale.

Consumer Sentiment Index

546

How do we calculate

We gather and analyze consumer sentiment from a range of sources to create the Consumer Sentiment Index to determine customer satisfaction levels for each feature outlined below. This data is designed to give you an idea of real consumer experience of the services and product we review. This data is currently separate from our overall rating out of 5

Insights Analyzed

#

Interest Rates and APR

For Interest Rates and APR

61% of people had positive sentiments

8% of people had neutral sentiments

31% of people had negative sentiments

61%

8%

31%

For Interest Rates and APR

61% of people had positive sentiments

8% of people had neutral sentiments

31% of people had negative sentiments

#

Customer Service

For Customer Service

22% of people had positive sentiments

8% of people had neutral sentiments

70% of people had negative sentiments

22%

8%

70%

For Customer Service

22% of people had positive sentiments

8% of people had neutral sentiments

70% of people had negative sentiments

#

Loan Terms and Flexibility

For Loan Terms and Flexibility

45% of people had positive sentiments

34% of people had neutral sentiments

21% of people had negative sentiments

45%

34%

21%

For Loan Terms and Flexibility

45% of people had positive sentiments

34% of people had neutral sentiments

21% of people had negative sentiments

#

Ease of Approval and Process

For Ease of Approval and Process

67% of people had positive sentiments

3% of people had neutral sentiments

30% of people had negative sentiments

67%

3%

30%

For Ease of Approval and Process

67% of people had positive sentiments

3% of people had neutral sentiments

30% of people had negative sentiments

PenFed personal loan borrowers gave the lender mixed reviews. Some appreciated the ease and speed of the application process, while others had issues with customer service, transparency and loan processing. Some borrowers also faced unexpected fees.

Pros & Cons

No origination or prepayment fees

Prequalification with a soft credit check

Allows for co-borrowers

Doesn’t operate branches in all states

Requires membership

Charges late payment fee of $29

Details

Eligibility:

Minimum credit score. Does not disclose

Minimum income. Does not disclose

Co-borrowers. Permitted

Customer service

We called PenFed to evaluate its customer service team’s responsiveness and found it to be one of the most helpful and efficient experiences among lenders on our list. While we waited one minute and 15 seconds to connect with a rep, they provided complete transparency for each of our questions.

PenFed’s team disclosed essential loan details like loan amounts, available interest rates, required documentation and loan approval times. They also shared information about potential fees and payment assistance options if repayment becomes challenging. We are impressed with PenFed’s willingness to share this information with prospective borrowers, which can improve the overall loan experience.

Best for Credit Card Debt Consolidation

Happy Money

4.1

Our ratings take into account loan cost, loan details, eligibility and accessibility, customer experience and application process. All ratings are determined solely by our editorial team.

Happy Money is a lender designed to consolidate high-interest credit card debt into lower-interest personal loans with predictable repayment schedules.

Why We Like It

Happy Money offers credit card debt consolidation loans from $5,000 to $40,000 and sends payments directly to creditors. The lender also advertises a low maximum interest rate—lower than most credit card APRs—making it a good option to consolidate credit card debt.

What We Don’t Like

Happy Money charges an origination fee of up to 5.5% and may be unable to consolidate bills that aren’t credit card debt.

The Consumer Sentiment Index from Forbes Advisor uses a proprietary weighting system designed by our subject matter experts. It evaluates thousands of consumer insights and reviews from leading online forums to determine customer satisfaction at scale.

Consumer Sentiment Index

1,928

How do we calculate

We gather and analyze consumer sentiment from a range of sources to create the Consumer Sentiment Index to determine customer satisfaction levels for each feature outlined below. This data is designed to give you an idea of real consumer experience of the services and product we review. This data is currently separate from our overall rating out of 5

Insights Analyzed

#

Interest Rates and Fees

For Interest Rates and Fees

79% of people had positive sentiments

6% of people had neutral sentiments

15% of people had negative sentiments

79%

6%

15%

For Interest Rates and Fees

79% of people had positive sentiments

6% of people had neutral sentiments

15% of people had negative sentiments

#

Customer Service

For Customer Service

79% of people had positive sentiments

1% of people had neutral sentiments

20% of people had negative sentiments

79%

1%

20%

For Customer Service

79% of people had positive sentiments

1% of people had neutral sentiments

20% of people had negative sentiments

# 3

Loan Terms and Flexibility

For Loan Terms and Flexibility

53% of people had positive sentiments

9% of people had neutral sentiments

38% of people had negative sentiments

53%

9%

38%

For Loan Terms and Flexibility

53% of people had positive sentiments

9% of people had neutral sentiments

38% of people had negative sentiments

#

Ease of Approval and Process

For Ease of Approval and Process

93% of people had positive sentiments

1% of people had neutral sentiments

6% of people had negative sentiments

93%

1%

6%

For Ease of Approval and Process

93% of people had positive sentiments

1% of people had neutral sentiments

6% of people had negative sentiments

Happy Money borrowers express mixed feelings about its personal loans. While many appreciate the streamlined application, quick approvals and competitive interest rates, others report poor communication, difficulties with payment adjustments and frustrations with the online platform.

Pros & Cons

Pays creditors directly

Offers low rates

No late fees, returned check fees or prepayment penalty fees

Has origination fees

Primarily consolidates credit card debt

Doesn’t allow co-signers or co-borrowers

Details

Eligibility:

Minimum credit score. 640

Minimum income. None

Co-signers. Not permitted

Co-borrowers. Not permitted

Customer service

We tested Happy Money’s customer service quality to gauge a prospective borrower’s experience. Through our research, we found that Happy Money had the longest wait time, two minutes and 15 minutes, which may be frustrating for some customers.

Once we connected with a representative, they disclosed much of the information we hoped to receive. For example, they shared loan amounts, interest rates, required documentation and turnaround times for the entire loan process, including preapproval, approval and funding. Besides the wait time to speak with a representative, the call was helpful and effective.

Best for Traditional Banking

U.S. Bank

4.1

Our ratings take into account loan cost, loan details, eligibility and accessibility, customer experience and application process. All ratings are determined solely by our editorial team.

Minimum Credit Score

Does not disclose

APR range

8.74% to 24.99%

with autopay

Loan amounts

$1,000 to $50,000 for existing U.S. Bank customers and up to $25,000 for new customers

$1,000 to $50,000 for existing U.S. Bank customers and up to $25,000 for new customers

Depends on the area you live in

Editor’s Take

U.S. Bank is a traditional bank that operates branches in 26 states and is available to borrowers nationwide.

Why We Like It

For borrowers looking for a loan from a traditional bank, U.S. Bank’s personal loans stand out for having competitive interest rates and a range of loan amounts.

What We Don’t Like

U.S. Bank’s $50,000 maximum loan amount is available only to current customers.

Who It’s Best For

U.S. Bank personal loans are best for existing customers who live in one of the lender’s 26 states with branches.

Consumer Sentiment Index

2.6

2.6/10

Consumer Score

The Consumer Sentiment Index from Forbes Advisor uses a proprietary weighting system designed by our subject matter experts. It evaluates thousands of consumer insights and reviews from leading online forums to determine customer satisfaction at scale.

Consumer Sentiment Index

2,112

How do we calculate

We gather and analyze consumer sentiment from a range of sources to create the Consumer Sentiment Index to determine customer satisfaction levels for each feature outlined below. This data is designed to give you an idea of real consumer experience of the services and product we review. This data is currently separate from our overall rating out of 5

Insights Analyzed

#

Interest Rates and Fees

For Interest Rates and Fees

20% of people had positive sentiments

4% of people had neutral sentiments

76% of people had negative sentiments

20%

4%

76%

For Interest Rates and Fees

20% of people had positive sentiments

4% of people had neutral sentiments

76% of people had negative sentiments

#

Customer Service

For Customer Service

5% of people had positive sentiments

2% of people had neutral sentiments

93% of people had negative sentiments

5%

2%

93%

For Customer Service

5% of people had positive sentiments

2% of people had neutral sentiments

93% of people had negative sentiments

#

Loan Terms and Flexibility

For Loan Terms and Flexibility

36% of people had positive sentiments

21% of people had neutral sentiments

43% of people had negative sentiments

36%

21%

43%

For Loan Terms and Flexibility

36% of people had positive sentiments

21% of people had neutral sentiments

43% of people had negative sentiments

#

Ease of Approval and Process

For Ease of Approval and Process

31% of people had positive sentiments

3% of people had neutral sentiments

66% of people had negative sentiments

31%

3%

66%

For Ease of Approval and Process

31% of people had positive sentiments

3% of people had neutral sentiments

66% of people had negative sentiments

The majority of feedback for U.S. Bank was negative, with many borrowers expressing dissatisfaction with the customer service and issues with the loan process. Borrowers reported unexpected fees, delays and problems with loan payoff and documentation.

Pros & Cons

Operates physical branches

0.50% autopay discount

Quick funding

Need a credit score of at least 800 to qualify for the lowest advertised rates

Smaller loan amounts available to non-U.S. Bank checking customers

Branch locations in only 26 states

Details

Eligibility:

Minimum credit score. Does not disclose

Minimum income. Does not disclose

Co-signers. Permitted

Co-borrowers. Permitted

Customer service

We called U.S. Bank’s customer service team to test its quality. Compared to other lenders on our list, we waited the second longest for our call to be answered—two minutes and one second. Although the representative was friendly and transparent, they provided most of the information through a sales pitch, which may be unsettling to some prospective borrowers.

U.S. Bank was one of few lenders that provided a specific interest rate based on loan details we provided. While the rep didn’t ask for a credit score to provide the interest rate, its website discloses you need a score of at least 800 to qualify for the lowest rates.

Best for No Credit

Upstart

4.0

Our ratings take into account loan cost, loan details, eligibility and accessibility, customer experience and application process. All ratings are determined solely by our editorial team.

Upstart is an AI-based lending platform that evaluates loan applications using non-conventional variables, such as college education.

Why We Like It

Upstart makes personal loans available to many borrowers, including those without established credit histories. Borrowers with a credit score must have a score of at least 620, but borrowers without a credit score may also be approved if they meet other criteria.

What We Don’t Like

Upstart’s maximum advertised interest rate is higher than other lenders, and it charges an origination fee of up to 12%.

The Consumer Sentiment Index from Forbes Advisor uses a proprietary weighting system designed by our subject matter experts. It evaluates thousands of consumer insights and reviews from leading online forums to determine customer satisfaction at scale.

Consumer Sentiment Index

2,077

How do we calculate

We gather and analyze consumer sentiment from a range of sources to create the Consumer Sentiment Index to determine customer satisfaction levels for each feature outlined below. This data is designed to give you an idea of real consumer experience of the services and product we review. This data is currently separate from our overall rating out of 5

Insights Analyzed

#

Interest Rates and Fees

For Interest Rates and Fees

28% of people had positive sentiments

14% of people had neutral sentiments

58% of people had negative sentiments

28%

14%

58%

For Interest Rates and Fees

28% of people had positive sentiments

14% of people had neutral sentiments

58% of people had negative sentiments

#

Customer Service

For Customer Service

10% of people had positive sentiments

3% of people had neutral sentiments

87% of people had negative sentiments

10%

3%

87%

For Customer Service

10% of people had positive sentiments

3% of people had neutral sentiments

87% of people had negative sentiments

#

Loan Terms and Flexibility

For Loan Terms and Flexibility

56% of people had positive sentiments

16% of people had neutral sentiments

28% of people had negative sentiments

56%

16%

28%

For Loan Terms and Flexibility

56% of people had positive sentiments

16% of people had neutral sentiments

28% of people had negative sentiments

#

Ease of Approval and Process

For Ease of Approval and Process

66% of people had positive sentiments

8% of people had neutral sentiments

26% of people had negative sentiments

66%

8%

26%

For Ease of Approval and Process

66% of people had positive sentiments

8% of people had neutral sentiments

26% of people had negative sentiments

Upstart borrowers express frustration with high interest rates and origination fees that increase the cost of borrowing. While borrowers found Upstart’s borrowing process simple and quick, others reported issues with customer service, communication and lending practices.

Pros & Cons

Accessible to borrowers with no credit history

Prequalification with a soft credit check

Ability to choose a custom payment date

Charges an origination fee up to 12% of the loan amount

No co-signer option

Only offers three- or five-years terms

Details

Eligibility:

Minimum credit score. 620

Minimum income. No minimum but must have a source of income

Co-signers. Not permitted

Co-borrowers. Not permitted

Customer service

We tested Upstart’s customer service quality to evaluate its helpfulness. Through our research, we found Upstart’s team was one of the fastest to answer, as we waited only 39 seconds. However, once connected, the representative was vague. While they disclosed general loan details like loan amounts, fees and interest rate ranges, they were unclear about documentation requirements and approval times.

Best for Below Average Credit

LendingPoint

3.9

Our ratings take into account loan cost, loan details, eligibility and accessibility, customer experience and application process. All ratings are determined solely by our editorial team.

LendingPoint is an online lender that offers small personal loans to borrowers with damaged credit histories.

Why We Like It

With a minimum credit score requirement of 600 , LendingPoint makes loans available to borrowers with fair credit at potentially low interest rates.

What We Don’t Like

LendingPoint charges an origination fee of up to 10% and interest rates from 7.99% to 35.99% .

Who It’s Best For

LendingPoint’s personal loans are best for borrowers who have fair credit and can’t qualify for loans elsewhere, or borrowers who can qualify for the lowest advertised interest rates.

Consumer Sentiment Index

6.0

6/10

Consumer Score

The Consumer Sentiment Index from Forbes Advisor uses a proprietary weighting system designed by our subject matter experts. It evaluates thousands of consumer insights and reviews from leading online forums to determine customer satisfaction at scale.

Consumer Sentiment Index

10,607

How do we calculate

We gather and analyze consumer sentiment from a range of sources to create the Consumer Sentiment Index to determine customer satisfaction levels for each feature outlined below. This data is designed to give you an idea of real consumer experience of the services and product we review. This data is currently separate from our overall rating out of 5

Insights Analyzed

#

Interest Rates and Fees

For Interest Rates and Fees

64% of people had positive sentiments

13% of people had neutral sentiments

23% of people had negative sentiments

64%

13%

23%

For Interest Rates and Fees

64% of people had positive sentiments

13% of people had neutral sentiments

23% of people had negative sentiments

#

Customer Service

For Customer Service

68% of people had positive sentiments

2% of people had neutral sentiments

30% of people had negative sentiments

68%

2%

30%

For Customer Service

68% of people had positive sentiments

2% of people had neutral sentiments

30% of people had negative sentiments

#

Loan Terms and Flexibility

For Loan Terms and Flexibility

84% of people had positive sentiments

7% of people had neutral sentiments

9% of people had negative sentiments

84%

7%

9%

For Loan Terms and Flexibility

84% of people had positive sentiments

7% of people had neutral sentiments

9% of people had negative sentiments

#

Ease of Approval and Process

For Ease of Approval and Process

95% of people had positive sentiments

2% of people had neutral sentiments

3% of people had negative sentiments

95%

2%

3%

For Ease of Approval and Process

95% of people had positive sentiments

2% of people had neutral sentiments

3% of people had negative sentiments

Borrowers appreciate the easy application process and robust customer service but criticize the high interest rates and misleading prequalification process. Some borrowers are concerned about LendingPoint’s perceived predatory practices and poor handling of loans post-approval.

Pros & Cons

Quick funding

Low credit score requirements

No prepayment penalty

Origination fee up to 10%

Co-signers or joint loans not permitted

Not available in Nevada and West Virginia

Details

Eligibility:

Minimum credit score. 600

Minimum annual income. $35,000

Co-signers. Not permitted

Customer service

After testing and evaluating LendingPoint’s customer service, we found it to be one of the most helpful and transparent lenders on our list after waiting only 46 seconds to be connected to a representative. The customer service representative we spoke with shared an in-depth perspective of their loan offers, including information about loan amounts, eligibility requirements, how interest rates are determined and prequalification.

LendingPoint’s team also disclosed late fees but didn’t confirm origination fees. While customer service didn’t share this information wasn’t, the lender discloses a fee of up to 10% on its website. LendingPoint was also one of few lenders that shared how they report payments to credit bureaus, which it typically does at the start of the month.

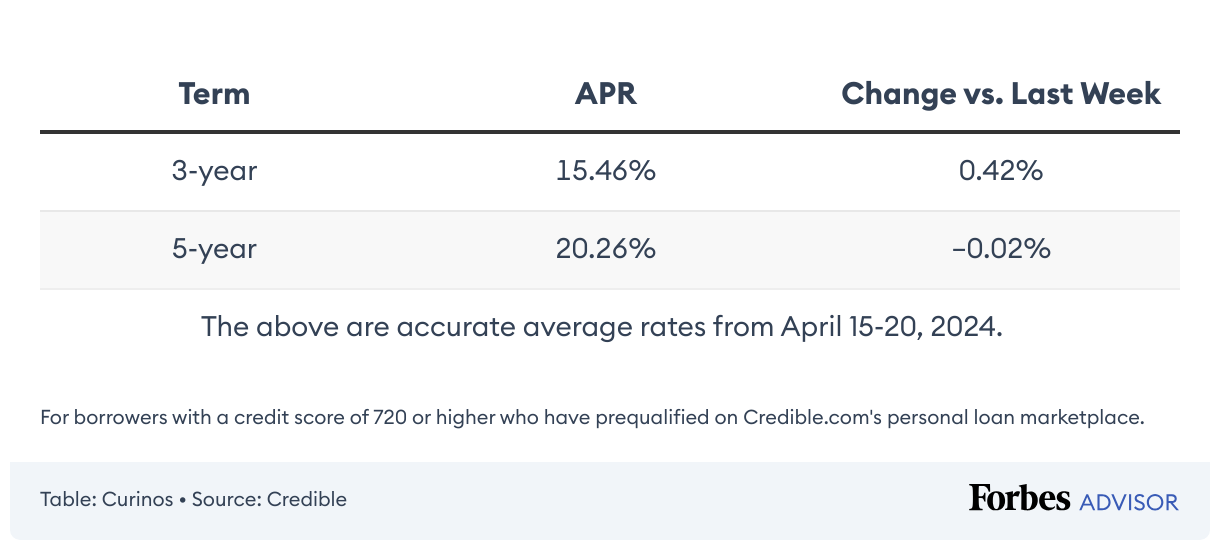

The above personal loan rates are accurate as of March 3, 2025. Some APRs and loan amounts are available for certain loan purposes.

Compare Personal Loan Options

As you shop for a personal loan, it can be difficult to narrow down your options. The first step to being able to compare your options is to prequalify with the lenders that may work best for you. Prequalification doesn’t impact your credit score and can give you an idea of the rates, terms and loan amounts you could be offered.

Once you have your prequalification offers, use these loan features to find the best personal loan for your financial situation.

Annual Percentage Rate (APR)

A loan’s APR includes both interest and standard fees, and is the cost of borrowing money. To find the lowest-cost loan, look for the lowest interest rate or APR offered to you. Keep in mind that although APR can help determine which loan is best for you, other loan features can help narrow down your options.

Fees

Loan fees vary by lender, and while some may be included in the APR—such as origination fees—there are other separate fees. For instance, some lenders don’t charge late fees for late payments and others don’t charge prepayment penalties if you repay your loan early. If you could be charged either of those fees during repayment, it may be best to find a lender that won’t penalize you for that.

Loan Amounts

Each lender advertises different loan amount ranges and the loan amount lenders offer to you could also be different from what you request. If that’s the case, eliminate the lenders that don’t offer the loan amount you need to cover your financial needs.

Perks

Perks are another feature that can be used to compare your loan options. Some lenders offer interest rate discounts if you sign up for autopay, and lenders may also offer direct payment to creditors for debt consolidation loans.

Terms

The time you’re given to repay a loan, or term, will vary by lender. As you consider your options, look for lenders offering loans with terms that work for you and your budget. A loan calculator can help determine the payments and terms you can afford.

Ask an expert

What should prospective borrowers consider when choosing a personal loan?

Joel Larsgaard

Advisory Board Member

Tom Thunstrom

Advisory Board Member

Taylor Medine

Mortgages & Loans Writer

The first thing to consider is whether or not you need one in the first place.

Personal loans are often used to fuel consumption or consolidate debt, but that comes at a cost. Instead of taking out a personal loan to go on vacation, consider saving up longer to pay for it in cash! And while a personal loan might make sense on the debt consolidation front, it could also prolong or exacerbate the problem, keeping you in debt for a longer period of time.

A focused plan of attack to pay off your debt is often better than moving that debt around, opting for different debt vehicles. But if you’re able to use a personal loan as a tool to help you eradicate high-interest debt quickly, it can make financial sense.

Just make sure you shop around and do business with a reputable lender. Read the fine print so you know what fees and penalties to expect, too.

If you are thinking about a personal loan, consider these factors:

Is there another way to borrow funds? For instance, if you own a home, can you utilize a home equity loan or line of credit? If you have a 401k plan, will your provider allow you to borrow against the plan for a short-term need? Both of these likely will provide a lower interest rate than an unsecured personal loan.

How is your credit? If you have fair to poor credit, utilize a nonprofit credit counseling service to help you address past credit issues and develop a plan to improve your credit score. Ask your local bank or credit union if you’re unsure who to contact. You can also utilize these steps to improve your credit before you apply for any loan.

Can you incorporate the payment into your monthly budget? Regardless of the personal loan option you choose, you will have an expense to repay over time. Can you make that payment?

My rule for loan shopping is similar to shopping for a car, couch, mattress or any other big-ticket item: Never take the first offer without haggling or looking elsewhere.

Doing a bit of lender sleuthing online and negotiating offers is the best way to uncover deals, discounts and rate-beat programs that could save you money.

Before agreeing to a loan, it’s also crucial to make sure you can handle loan payments—with money to spare. Sure, personal loans can be a shortcut to zero out your credit card balance and pay for a big expense (hello, dental work, bathroom renos, cross-country moves and more).

But agreeing to payments of, say, $500 or $1,000, over a one- to five-year period is a huge commitment, and falling behind can put you in a very sticky situation. Only borrow what you need and pay attention to how interest affects monthly and long-term payments before signing.

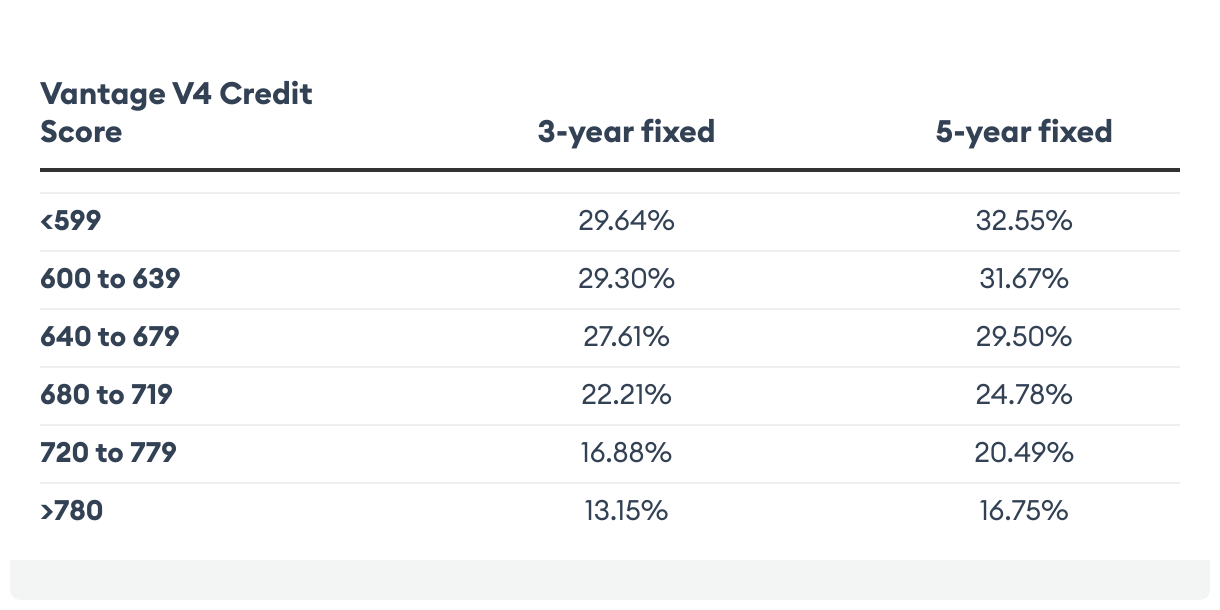

Personal loan interest rates fluctuate frequently and can vary by loan term. Although you may not be offered the current average rates, they can help determine what you can expect.

Average Personal Loan Interest Rates by Credit Score

Lenders use your credit score to determine how risky it is to lend money to you. The lower your credit score, the higher your risk—and as a result, the more likely it is that any loan offers will have high interest rates.

Pros and Cons of Personal Loans

Before getting a personal loan, it’s important to consider the pros and cons.

PROS

CONS

Fixed, predictable payments

High interest rates

Can lower interest rates with debt consolidation

Long terms can make repayment difficult

Can help build your credit

Fees and other charges

Can be used for nearly any expense

Can require collateral

Fast funding turnaround

Can damage your credit

How To Qualify for a Loan

Lenders use several different factors to determine whether or not you’re eligible for a loan. To qualify for a loan, you’ll need to meet certain requirements for each of these categories.

Credit score. Lenders will look at your credit score and history to determine how you’ve handled debt in the past. To qualify for most personal loans, you’ll need a credit score of 600 or higher.

Income. Lenders will use your income to evaluate your ability to repay a loan. In many cases, lenders don’t disclose exact income requirements but do require enough income to cover loan payments. Lenders consider traditional income along with other forms, such as alimony, government assistance and child support.

Debt-to-income (DTI) ratio. Your DTI compares your income to your current debt payments. This shows lenders if you can afford additional debt payments with your current income. Often, lenders look for a DTI of less than 36%.

Collateral. If you’re applying for a secured loan, you’ll need sufficient collateral to back your loan. This can be a car, your 401(k) or other assets. Keep in mind that if you fail to repay a secured loan, your lender can take possession of the collateral as loan repayment.

How To Apply for a Personal Loan

If you’re looking to apply for a loan, follow these steps:

Check your credit. The first step to getting a loan is checking your credit report. Make sure there aren’t any errors on it, and if there are, contact the three major credit bureaus to correct any mistakes. You can use your credit to help determine which lenders may work with you.

Determine financial need. A crucial part of getting a loan is determining how much money you need to borrow. This can help you narrow down which lenders to apply with, but it can also help prevent over-borrowing. Along with a loan calculator, you can find the terms and amounts that work for you.

Shop around. Once you know your qualifications, such as credit and income, find lenders where you’ll meet the eligibility requirements and that offer the loan you’re looking for.

Prequalify. Prequalifying with a personal loan lender can give you an idea of the rates and terms you could be offered without impacting your credit. This can help you make a decision on which lender works best for you before submitting a loan application.

Submit an application. Once you’ve found the best lender for you, gather any necessary documentation such as proof of identity, income verification and proof of address. Then, you can submit an application.

Begin repayment. If a lender approves your application, you can then accept the loan amount. Once you do that, you’ll receive the loan and begin repayment. Setting up autopay can help make sure you won’t miss any payments.

Alternatives to a Personal Loan

Although a personal loan can be an effective tool to cover an emergency expense, it may not be right for everyone. Before getting a personal loan, consider the alternative funding options available to you.

Payday alternative loan. Payday alternative loans (PAL) are available from some credit unions in amounts up to $2,000. Interest rates on these loans are capped at 28%, and loan terms can reach up to six months.

Home equity financing. If you’ve established equity in your home, a home equity loan or home equity line of credit (HELOC) can be a cheaper financing option compared to personal loans. Keep in mind, these financing options are secured by your home, so if you default, your lender can take possession of your home.

Credit cards. If you need to cover a short-term financial emergency with a small amount of money, a credit card can be an effective tool if you have a plan to repay your debt. Since credit cards carry high APRs, if you don’t repay your debt by the end of your statement period, you can start accumulating interest and fees quickly.

Cash advance app. Cash advance apps offer small sums of money with short repayment terms. If repaid on time, these cash advances can have minimal costs, but if you miss a payment, fees can add up quickly.

Friends and family. If you have friends or family that you can borrow money from, this can be the cheapest and most efficient way to cover a financial emergency. If you do borrow money from a loved one, be sure to write up a promissory note outlining the loan terms so you both have the same expectations on repayment.

Methodology

We reviewed 31 popular lenders based on 16 data points in the categories of loan details, loan costs, eligibility and accessibility, customer experience and the application process. We chose the best lenders based on the weighting assigned to each category:

Loan costs. 35%

Loan details. 20%

Eligibility and accessibility. 20%

Customer experience. 15%

Application process. 10%

Within each major category, we also considered several characteristics, including available loan amounts, repayment terms, APR ranges and applicable fees. We also looked at minimum credit score requirements, whether each lender accepts co-signers or joint applications and the geographic availability of the lender. Finally, we evaluated each provider’s customer support tools, borrower perks and features that simplify the borrowing process—like prequalification options and mobile apps.

Where appropriate, we awarded partial points depending on how well a lender met each criterion.

A good interest rate on a personal loan is one that’s lower than the national average for borrowers with excellent credit. However, the interest rate you receive depends on several factors, and lenders frequently charge other fees that can make a loan more expensive. To minimize costs, maintain a good to excellent credit score (at least 670).

How many personal loans can you have at once?

You may have more than one personal loan with one specific lender or multiple loans with different lenders. However, some lenders may set a limit to how many loans you can have open through them, such as two loans. Plus, opening multiple loans can make you appear as a riskier borrower and lower your qualification chances.

How long does it take to get a personal loan?

Typically, it doesn’t take long to get a personal loan. Some lenders offer online applications with automated approvals and same-day funding. Most lenders, however, take a few business days to a week to process your application and disburse your funds.

If the lender needs to verify any information with you, it can take longer. Once you apply for a loan, look for any communication from your lender so you can respond promptly.

Information provided on Forbes Advisor is for educational purposes only. Your financial situation is unique and the products and services we review may not be right for your circumstances. We do not offer financial advice, advisory or brokerage services, nor do we recommend or advise individuals or to buy or sell particular stocks or securities. Performance information may have changed since the time of publication. Past performance is not indicative of future results.

Forbes Advisor adheres to strict editorial integrity standards. To the best of our knowledge, all content is accurate as of the date posted, though offers contained herein may no longer be available. The opinions expressed are the author’s alone and have not been provided, approved, or otherwise endorsed by our partners.

Colin Beresford is a writer and editor experienced in helping people make the best decisions with their money, whether it's buying a car or taking on a loan. He has written for Bloomberg, The Associated Press, NerdWallet, Car and Driver magazine, among many others covering various financial topics.

Jordan Tarver has spent seven years covering mortgage, personal loan and business loan content for leading financial publications such as Forbes Advisor. He blends knowledge from his bachelor's degree in business finance, his experience as a top performer in the mortgage industry and his entrepreneurial success to simplify complex financial topics. Jordan aims to make mortgages and loans understandable.

Financial and loans expert Joel Larsgaard loves nerding out on the topic of personal finance with the mission of helping others improve their financial standing.

He has been in the money media space for almost 20 years. He produced "The Clark Howard Show" for 14 of those years and has been hosting the "How To Money" podcast for six years. He currently hosts “How To Money”—which has covered debt, loan options and related subjects—three times a week, and a personal finance radio show on KFI radio in Los Angeles on Sunday afternoons. Basically, he's been marinating in all things personal finance for a long time.

His goal is to help his cadre of listeners live a balanced life, saving and investing for their future while simultaneously enjoying the here and now. Joel's other passions include sipping delicious craft beer, riding bikes, and exploring Atlanta with his wife and three kids.

Was this article helpful?

Send feedback to the editorial team

Thank You for your feedback!

Something went wrong. Please try again later.

The Forbes Advisor editorial team is independent and objective. To help support our reporting work, and to continue our ability to provide this content for free to our readers, we receive compensation from the companies that advertise on the Forbes Advisor site. This compensation comes from two main sources. First, we provide paid placements to advertisers to present their offers. The compensation we receive for those placements affects how and where advertisers' offers appear on the site. This site does not include all companies or products available within the market. Second, we also include links to advertisers' offers in some of our articles; these “affiliate links” may generate income for our site when you click on them. The compensation we receive from advertisers does not influence the recommendations or advice our editorial team provides in our articles or otherwise impact any of the editorial content on Forbes Advisor. While we work hard to provide accurate and up to date information that we think you will find relevant, Forbes Advisor does not and cannot guarantee that any information provided is complete and makes no representations or warranties in connection thereto, nor to the accuracy or applicability thereof. Here is a list of our partners who offer products that we have affiliate links for.