Compare Life Insurance Quotes

Best Life Insurance Companies

- Pacific Life – Best Overall

- Protective – Best for Indexed Universal Life Insurance

- Prudential – Great for Reliable Policy Illustrations

- Lincoln Financial – Great for Variable Universal Life Insurance

- MassMutual – Best for Financial Strength

- Nationwide – Great for Young Adults

- Mutual of Omaha – Best for Investment Performance

- Penn Mutual – Best for Universal Life Insurance

Best Term Life Insurance Companies

We found that Corebridge Financial, Pacific Life, Protective and Symetra offer the best term life insurance. Term life insurance is ideal for covering finite financial concerns, like the years until retirement.

Best Universal Life Insurance Companies

Penn Mutual is the best universal life insurance company in our analysis. Universal life insurance offers the flexibility of adjustable premium payments, within certain parameters, and a flexible death benefit amount.

Best No-Exam Life Insurance Companies

Brighthouse Financial, Legal & General America, Pacific Life and Transamerica are the best companies in our no-exam life insurance analysis. No-exam life insurance offers the convenience of skipping the medical exam typically required by traditional life insurance.

Cheapest Life Insurance Companies

Symetra is our top pick for the cheapest life insurance company, based on our analysis of term life insurance rates.

How Do I Choose the Best Life Insurance?

Tony Steuer

Advisory Board Member

Ashlee Valentine

Insurance Editor

Amy Danise

Insurance Managing Editor

Establish your financial goals

Once you know your goals, then find the policy that’s right for you. An experienced life insurance agent can help you find the right company and policy. Insurance companies vary in their underwriting criteria and pricing, so while one company can be good for one person, another company might be better for you.

Advisory Board Member

Check financial strength ratings

I always make sure the companies I’m considering have an A rating or higher for financial strength. These ratings are available from agencies like AM Best and Standard & Poor’s and help me identify companies that will be able to pay claims many years in the future. That’s why all the companies in our analysis are rated A or higher.

Insurance Editor

Work with experienced professionals

I’ve found it’s essential to work with an experienced life insurance agent or financial advisor who knows which insurers are most likely to give the best price based on age and health. You want to know if you have a good chance of getting a decent quote from an insurer before you apply. A good life insurance agent or financial advisor can also anonymously shop around for you, so you don’t get declined—which can affect your ability to buy life insurance later from someone else.

Insurance Managing Editor

How Much Does a Life Insurance Policy Cost?

Here is the average cost of life insurance for different types of policies, though your own life insurance rates will depend on your age, health, gender, amount of coverage and more.

- Term life insurance costs an average of $217 a year, or $18 a month, for a 30-year-old woman for a 20-year, $500,000 term life insurance policy, based on the companies in our analysis. For a male buyer of the same age, the same policy costs an average of $257 a year or $21 a month.

- Whole life insurance costs an average of $3,945 a year, or $329 a month, for a 30-year-old woman with $500,000 coverage. For a male buyer the same age, the same policy costs an average of $4,375 a year or $365 a month.

Life Insurance Cost for Females

Here are the average monthly costs for each top-ranking life insurance company for a 20-year $500,000 term life insurance policy for a healthy female.

| Company | Buyer age 30 cost per month | Buyer age 40 cost per month | Buyer age 50 cost per month |

|---|---|---|---|

| $16 | $23 | $53 | |

| $16 | $24 | $54 | |

| $21 | $29 | ||

| $16 | $26 | $58 | |

| $19 | $28 | $61 | |

| $19 | $26 | $55 | |

| $20 | $28 | $61 | |

| $15 | $23 | $53 |

Life Insurance Cost for Males

Here are the average monthly costs for each top-ranking life insurance company for a 20-year $500,000 term life insurance policy for a healthy male.

| Company | Buyer age 30 cost per month | Buyer age 40 cost per month | Buyer age 50 cost per month |

|---|---|---|---|

| $18 | $28 | $68 | |

| $18 | $28 | $69 | |

| $24 | $33 | $71 | |

| $19 | $32 | $75 | |

| $23 | $31 | $80 | |

| $22 | $30 | $74 | |

| $22 | $33 | $82 | |

| $18 | $28 | $68 |

Life Insurance Policies Available by Company

| Company | Term life | Whole life | Universal life | Indexed universal life | Variable universal life | Guaranteed universal life |

|---|---|---|---|---|---|---|

| ✓ | ✓ | ✓ | ✓ | ✓ | ✖ | |

| ✓ | ✓ | ✓ | ✖ | ✓ | ✖ | |

| ✓ | ✓ | ✖ | ✓ | ✖ | ✖ | |

| ✓ | ✖ | ✖ | ✓ | ✓ | ✓ | |

| ✓ | ✓ | ✓ | ✖ | ✓ | ✖ | |

| ✓ | ✓ | ✖ | ✓ | ✓ | ✓ | |

| ✓ | ✓ | ✓ | ✓ | ✖ | ✖ | |

| ✓ | ✓ | ✖ | ✓ | ✓ | ✓ |

Related: How To Get Life Insurance

We Answer Your Questions

Amy Danise

Insurance Managing Editor

Les Masterson

Insurance Editor

Michelle Megna

Insurance Lead Editor

I’m a skydiving hobbyist. Will this impact my life insurance options?

– John R., Cincinnati, Ohio

Insurers consider your risk of dying while skydiving to be significantly higher than if you did not skydive, and, therefore, they may give you higher quotes or deny your application entirely. Honesty is always best when it comes to life insurance, so do not be dishonest about your hobby. Instead, work with an independent agent to find insurers that are most likely to offer the best quotes for high-risk life insurance.

Insurance Managing Editor

How can I ensure my life insurance death benefit is left to a charity after I’m gone?

-Agatha W., Lawrence, Kansas

There are a couple ways to donate your life insurance death benefit to a charity of your choice. You can name the charity as the beneficiary or transfer the ownership of the policy to a charity. There are pros and cons to each option. Check with the charity about its preference—it may not want to become the policy owner.

Insurance Editor

I’m 25 and have been told I shouldn’t spend money on life insurance right now because my odds of needing it are low. Am I too young to need life insurance?

-Abby M., Provo, Utah

Although your odds of dying are indeed low at 25, the best time to buy life insurance is when you’re young. Buying now allows you to lock in rates lower than you’ll ever be eligible for again. With every year you age, the rates you qualify for will be higher, and your odds of developing medical conditions will increase, which will also increase your rates when you buy a policy. Of course, it’s up to you if it makes financial sense to lock in at a low rate now.

Insurance Lead Editor

Compare Life Insurance Companies

Compare Policies With Leading Insurers

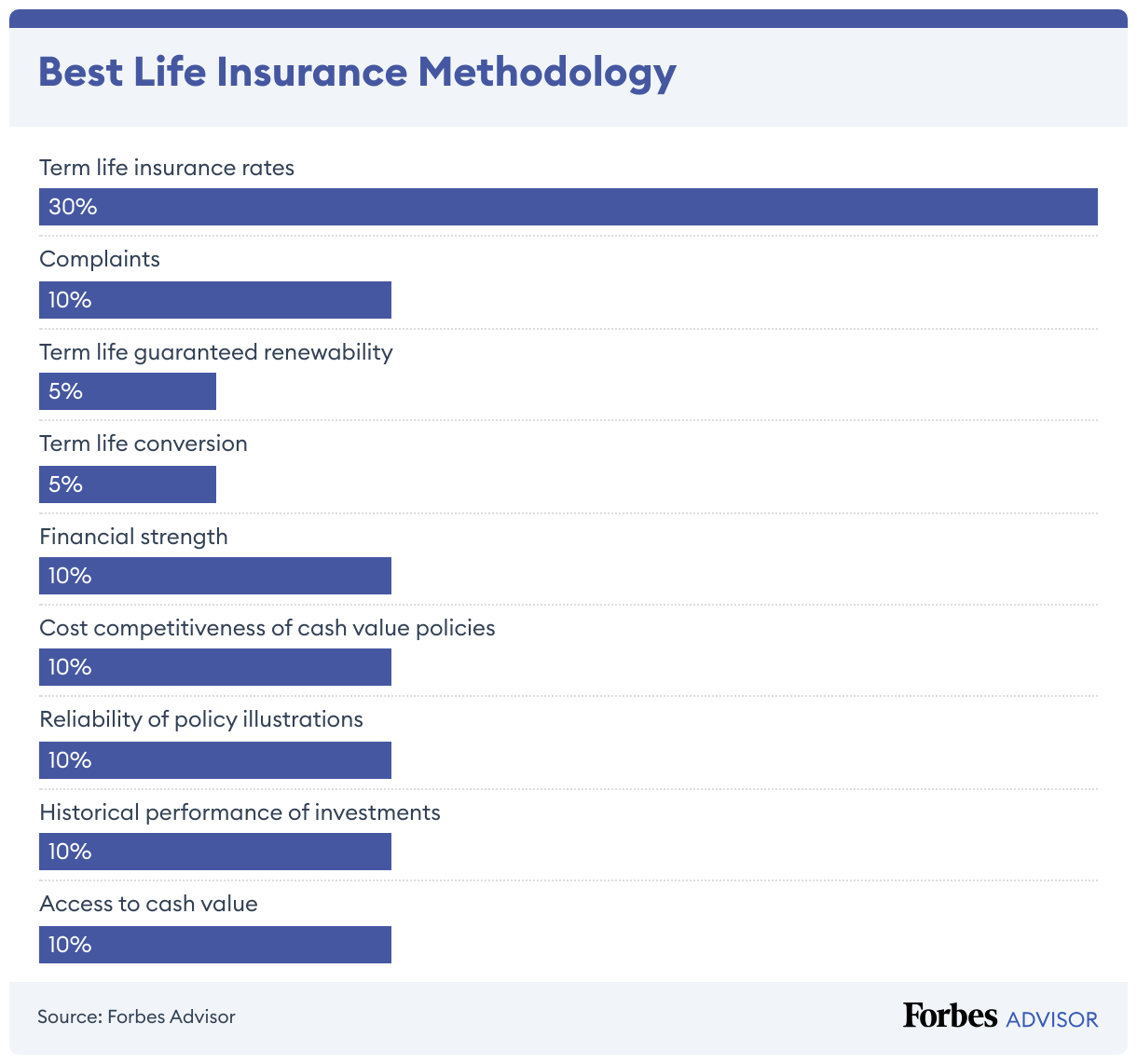

Methodology

To find the best life insurance companies, we evaluated term life and permanent life insurance for each company. We used our own research and data courtesy of Veralytic, a leading publisher of life insurance product research. Veralytic’s data provides a unique depth to Forbes Advisor’s analysis of whole, universal, indexed universal and variable universal life insurance policies from each insurer.

While independent research is commonplace for most every other element of our financial lives, life insurance product recommendations are too often based on hypothetical quotes or illustrations. What you pay in premiums and what you get in cash value and death benefits depends on what the insurance company actually charges and what you actually receive in performance over time. As such, Veralytic measures the competitiveness of internal policy costs and actual historical performance. Veralytic reports are available through financial advisors.

Our analysis was based on the following.

Looking For Life Insurance?

Compare quotes from participating carriers

Read more: How Forbes Advisor Rates Life Insurance Companies

Other Life Insurance Companies We Rated

| Company | Forbes Advisor rating |

|---|---|

| Columbus Life |   |

| Minnesota Life | |

| Guardian Life | |

| Midland | |

| Symetra | |

| Massachusetts | |

| Ameritas |  |

| National Life | |

More Life Insurance Ratings

If you’re looking for a specific type of policy, check out our top picks across these categories:

Best Life Insurance Companies Frequently Asked Questions (FAQs)

What does life insurance cover?

Life insurance covers the life of the insured person. If you pass away with an in-force life insurance policy, the beneficiaries specified on the policy will receive the death benefit. Beneficiaries can use that payout in any way they choose.

What does life insurance exclude?

Life insurance policies typically include a suicide clause. This clause specifies that suicide within the first two years of the policy will not be covered.

Apart from the suicide clause, life insurance policies pay the death benefit no matter the cause of death unless the insurer can prove misrepresentation or the policyholder stops paying premiums. An insurer may deny a life insurance claim if it discovers something like a known health issue that was not disclosed in the application. It could also deny a payout if the policy had lapsed due to nonpayment.

Can I buy life insurance on someone else?

Yes, you can purchase life insurance on someone else as long as you can prove an “insurable interest” in that person. An insurable interest means that you would financially suffer if they died. The person being insured must sign the application. You cannot purchase a policy on someone without their knowledge.

If you buy life insurance on someone else, you can make yourself the life insurance beneficiary.

Can I use my life insurance while still living?

If you have a cash value life insurance policy, there are ways to use your life insurance while still living. You can access the cash value through loans, withdrawals or by surrendering the policy.

Another way to use your life insurance while still living is through living benefits if your policy includes them. Living benefits allow you to access money from your own death benefit if you meet specific health requirements. This could include people who are diagnosed with a terminal, chronic or critical illness.

If you’re buying life insurance, find out what living benefits can be included in the policy.